Sam TV

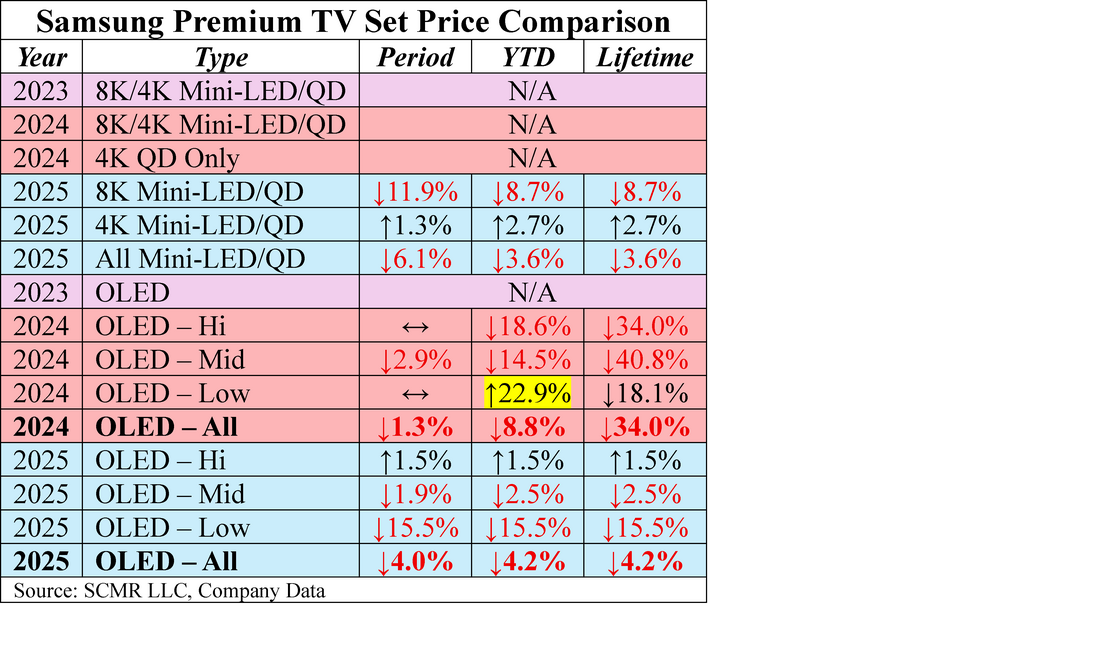

Given the lack of holidays or special events over the last 45 days, we have not checked Samsung Electronics (005930,KS) TV set pricing until today. It seems that Samsung has made some structural changes to their premium TV set availability and pricing during that period, essentially eliminating all 2024 8K Mini-LED/QD sets from their on-line roster and almost all (3 hi-end sets still available) Mini-LED/QD 4K sets for which they raised prices substantially. This is rather unusual as the previous year’s sets are typically available for at least the entire following year as an alternative for those looking to save money by purchasing last year’s models, but in this case Samsung pushes potential 2024 model purchasers to outside sources or to 2025 models. We note also that in 2024 Samsung made available 8K and 4K Mini-LED/QD sets along with a line of QD only sets, however this year they have eliminated the QD only line, meaning all LCD display premium TVs are Mini-LED/QD, with no alternative without the Mini-LED option.

In terms of OLED, Samsung seems to be taking the same track on last year’s models, eliminating all of the hi-end and low-end models, leaving only the mid-tier. Essentially pushing potential buyers to 2025 models. We note that 2024 low-end models saw a large price increase in May (from $2,000 to $3,400) but we are suspect about that change as that model has now been discontinued. Without that change the 2024 OLED low-end tier would be down 41.2% (lifetime), rather than down 18.1% and flat YTD (yellow highlight).

Over the last 49 days here is how Samsung’s on-line premium TV set pricing has evolved:

In terms of OLED, Samsung seems to be taking the same track on last year’s models, eliminating all of the hi-end and low-end models, leaving only the mid-tier. Essentially pushing potential buyers to 2025 models. We note that 2024 low-end models saw a large price increase in May (from $2,000 to $3,400) but we are suspect about that change as that model has now been discontinued. Without that change the 2024 OLED low-end tier would be down 41.2% (lifetime), rather than down 18.1% and flat YTD (yellow highlight).

Over the last 49 days here is how Samsung’s on-line premium TV set pricing has evolved:

All in, it seems that Samsung is taking an unusual turn with the premium TV set line this year, pushing buyers to 2025 models directly, rather than giving them the option of last year’s models and doing a little less anticipatory discounting in front of the Labor Day holiday. The exception seems to be the low-end of this year’s OLED line, where prices dropped over 15% during the period and remain far below the mid and upper tier OLED sets. There is the possibility that Samsung is able to capture any cost savings on the QD/OLED panels it uses for most of the low-end S85F models, but that is unconfirmed. We expect some additional discounting before the holiday itself.

RSS Feed

RSS Feed